Valuing Roof Spaces for Development

Friday, 13th September 2013

Party Walls | Surveying | Valuation

I’ve had to prepare a couple of valuations recently for owners that wanted to either buy or sell a roof space.

The most common scenario is where a property has been converted but the roof space, or part of it, has been retained by the freeholder; often for the purpose of housing cold water storage tanks serving the flats below. As the flats update their heating and hot water systems they will often switch to a combination boiler which runs off mains pressure and removes the need for a cold water tank.

The leasehold owner of the top floor flat will often spot an opportunity to extend their property and approach the Freeholder with a view to purchasing the space. It is at that point that we get the call to provide a valuation.

The first point to establish is whether the space could be sold on the open market or is only of use to the leaseholder of the adjacent demise. Points to consider are whether there would be a means of access if the space were to be developed as a separate dwelling and even if there was is the development viable from a planning point of view? The cost of complying with Building Regulations may also make the cost of developing a new dwelling too expensive.

In most cases the development will only be viable as an extension to the top floor flat so that will be the focus of the remainder of this post.

The definition of ‘market value’ is as follows:

The estimated amount for which an asset should exchange on the date of valuation between a willing buyer and a willing seller in an arm’s length transaction after proper marketing wherein the parties had each acted knowledgeably, prudently and without compulsion.

As there is only one potential purchaser in this scenario it will not be possible to properly market the roof space. We are therefore not looking to provide a market value.

The approach that we adopt is one of added value. The principle is the same as when a leaseholder pays compensation to their Landlord in return for granting an extension to the term of their lease. Once the existing term of the lease is added to the additional term which has been granted by the Landlord the property become more valuable. The term used is ‘marriage value’ and the Act covering lease extensions dictates that it is split equally between the parties.

When a leaseholder of a flat combines their demise with a roof space to form a larger property that larger property will be worth more than the combined value of the two separate spaces. There is no Act that requires the added value, or marriage value, to be split equally between the parties but it is considered to be the fairest method.

Methodology

The methodology that I would adopt to establish the marriage value is therefore the estimated market value of the top floor leasehold flat following its extension in to the roof space minus the current market value of the existing top floor leasehold flat combined with the cost of the necessary work (and some possible other factors).

The cost of the work should include any alterations that are necessary to the communal areas or any of the other leasehold flats in the building and professional fees including the estimated costs of complying with the Party Wall etc. Act 1996.

In addition to this there are any number of other considerations that could be added, depending on the level of detail of your report or inclination of your surveyor. The most common is a risk deduction, followed by costs of finance.

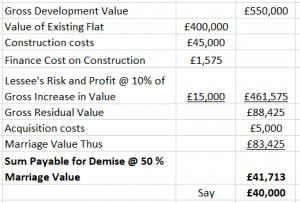

A valuation summary could look like this:

Now the example above is far from exhaustive in terms of detail, but would be a relatively typical example. Lessee’s risk and profit is perhaps a controversial one but is representative of the fact that the leaseholder is shouldering all the risk in this development, whilst the freeholder is exposed to none. If the premium for the loft space is paid in advance of the works being completed (and it usually is), then the project has to run precisely to plan, time and cost for the valuation to be correct. The 10% downwards adjustment reflects the likelihood of the project coming in at more than would have been expected. Of course the chance of the build coming in under budget and the contactor offering a nice healthy discount are slim to none!

There is a lot of subjective opinion when it comes to valuations of this type, so it is not unusual for both the leaseholder and the freeholder to instruct their own separate surveyors and to have a period of negotiation. Other freeholders are more relaxed and are happy to commission only one surveyor and one report. In that instance it is preferable for the Valuer to clearly state in his T&Cs, both leaseholder and freeholder as the client and that the report represents his impartial opinion.

Peter Barry undertake numerous valuations of this type and are experts in the field. The majority are undertaken by Matthew Price BSc MRICS and Steve Hobbs BSc MRICS. If you have any queries or questions further to this post please do not hesitate to contact us at surveying@peterbarry.co.uk or call us on 020 7183 2578.